2022 was another year to forget for the gold developers on balance, with several names suffering 50% plus drawdowns from their highs, and many companies with more marginal projects have seen even larger corrections. This represented a significant underperformance vs. gold producers which significantly outperformed the major market averages. Unfortunately, for the juniors, outside of some specific examples of clear disappointments and under-promising on plans (or capex blowouts), it's been very difficult for companies to buck this trend despite the calibre of news coming out of their projects. I believe this is partially due to sentiment being so poor that the fundamentals essentially went out the window, but also that the backdrop for juniors has rarely ever been worse and most names were painted with a similar brush.

The negatives for these developers are numerous and are as follows:

- a tight labor market

- inflationary pressures

- rising contractor costs

- a risk-off environment

- low equity prices

For a segment of the sector that must regularly raise capital (explorers/developers), these developments are not ideal given that it means that each dollar is going less far (higher costs to drill, higher contractor costs in other areas, and higher build costs), and economics have become less robust due to the sharp increase in build costs. Worse, each dollar is being raised at a fraction of the value that some shareholders and management might have hoped due to the risk-off environment. The result being that the companies will see more dilution than shareholders might have previously assumed, and in some cases, these projects are less robust due to having to sell royalties on their flagship project is equity prices were so low that it made little sense to raise capital in this manner due to the dilutive nature. Unfortunately, while a higher gold price does fix some of these issues, we have not seen anywhere near the advance in gold prices to compensate for a minimum of 30% inflation for most greenfields projects relative to 2020 levels.

Given that Skeena Resources (SKE) is a developer with a significant capex bill ahead (even if relatively small compared to expected annual and total output), it's not overly surprising that the stock was caught up in the violent correction sector-wide, and it finished 2022 as one of the worst performers, down 49% for the year. However, there are two key points worth noting. The first is that much of this underperformance in 2022 was due to significant outperformance in 2020, with the stock trouncing the performance of ASA, sporting a 428% return vs. ASA's 60% return. Secondly, while Skeena may be a developer which places it in a less attractive portion of the sector (especially when capex blowouts have become the norm, not the exception), the company has a very unique project in Eskay Creek.

This is because not only is it a world-class project that could be one of the highest grade open-pit mines globally post-2025, but it's located in a Tier-1 jurisdiction (Golden Triangle, British Columbia), it sits in close vicinity to existing infrastructure (hydro-electric power 17 kilometers away, Highway 37), and it stands out as being a brownfields site, with this being a historical mine under Barrick Gold (GOLD) that produced over 3.2 million ounces of gold and 162 million ounces of silver. Finally, although the share price may not have responded as some had hoped, the company continues to see exploration success that should not only extend the mine life, but also improve project economics, with additional opportunities to extend the mine life that include Eskay's underground potential. Hence, I would argue that the current After-Tax NPV (5%) of ~$1.07 billion significantly understates the project's true value. Let's take a closer look at Skeena below:

(Source: Company Website)

All figures are in United States Dollars unless otherwise noted at an exchange rate of 0.76/1.00 CAD/USD.

Eskay Creek: A World-Class Project In A Tier-1 Jurisdiction

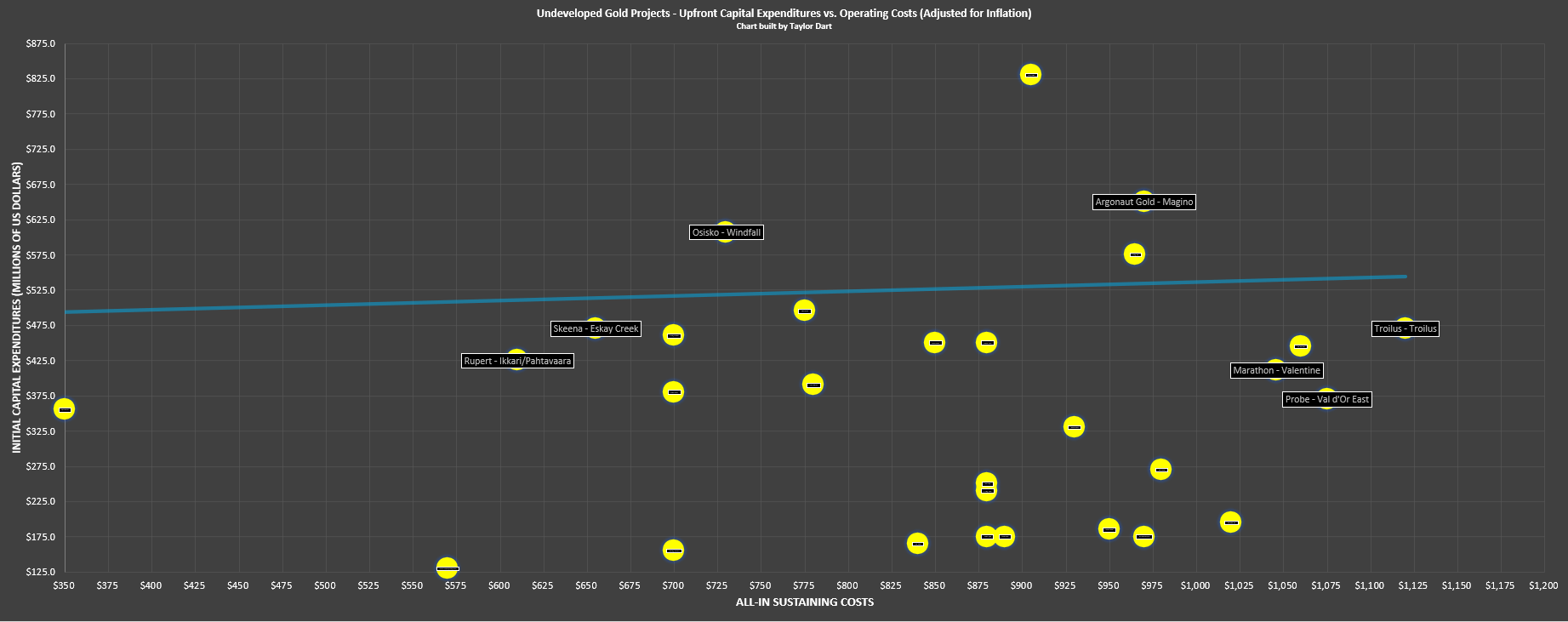

Skeena Resources is the proud owner of one of the most robust undeveloped gold projects globally, with the added favorable distinction of this project being located in a Tier-1 jurisdiction (Golden Triangle of British Columbia). The project's world-class economics were spelled out in the recently completed Feasibility Study, which highlighted an average production profile of ~352,000 gold-equivalent ounces [GEOs] over a 9-year mine life with multiple opportunities to extend this mine life and or optimize the mine plan based on recent drilling. However, it's not just the scale that makes Eskay Creek unique; it's the estimated operating costs and very modest upfront capex for a project capable of producing at this level. In fact, as the chart below shows, Eskay Creek would be one of the lowest-cost future gold mines (expected to begin production in H1 2026), with only a couple of projects having more attractive margins than Skeena, but these being less advanced, except for Skouries and Hod Maden in less favorable jurisdictions (Greece and Turkiye).

Meanwhile, from a capex standpoint, a ~$450 million capex bill is not low by any means, especially when this figure makes up nearly 100% of Skeena's current market cap. However, this is a very modest capex bill compared to companies pursuing a project of a similar size, and even Osisko's Windfall (OSK.TSX) is now expected to be a ~$600 million capex project for a relatively small footprint high-grade mine in northern Quebec. Some investors might roll their eyes at these capex figures since it's become difficult to trust these numbers with multiple capex blowouts in the past two years, including Cote, Valentine, and Magino, all in Canada. However, it's important to note that Skeena's study is based on relatively current cost estimates being completed in Q3 2022; it already has an existing and permitted tailings storage facility, and it's also a relatively small footprint project (~8,000 tonnes per day) relative to massive earth-moving projects and much larger processing plants at Cote and Magino. Hence, I don't think this is an unreasonable capex assumption, and a ~$35 million contingency is also baked in.

(Source: Company Filings, Author's Chart & Estimates)

In a period of high inflation and the potential for higher for longer inflation, I believe it makes sense to have an overweight position in producers and royalty/streaming companies vs. developers, given that they're less susceptible to capex blowouts (increasing production by leveraging off existing infrastructure in many cases). However, if one is interested in getting more leverage through gold developers, I believe it makes sense to focus on those names with projects in the bottom half and lower left of the above chart, given that they will maintain robust margins whether the gold price cooperates or not, they should see limited share dilution from any unexpected capex increases given that these increases will be less impactful from a dollar standpoint (vs. Cote, which saw a $1.0+ billion overrun), and they have the bonus upside of being highly attractive to gold producers which will see a significant increase in free cash flow generation if the gold price can stay above $1,900/oz and are actively looking for ways to claw back lost margins.

A clear example is Skeena, which has the unique benefit of being a brownfields site (less risk of a capex blowout) and having a very competent President & CEO at its helm, Randy Reichert, with considerable experience in operating assets (Kupol and Fekola), which could help with optimization and bringing Eskay Creek online on time and on budget. Notably, before being appointed VP of Operations for B2Gold (BTG), a major producer, Randy Reichert, was General Manager of Fekola, a similar high-grade open-pit project of a larger scale. (4.0 million tonnes per annum to start vs. ~2.9 million tonnes expected for Eskay Creek).

Recent Developments

In addition to exploration success which suggests an increase in ounces with newly discovered mineralization in the 21A West Zone and multiple solid intercepts outside of the planned pit in the 22 Zone, Skeena has also potentially added a completely new zone (the 23 Zone) which sits 200 meters east of the 21A Zone. This new discovery could positively impact Eskay Creek's project economics with an improved strip ratio, given its proximity to the Main Pit in the Feasibility Study. These positive drill results will all be incorporated into an updated resource estimate due in H1 of this year and should complement an already robust mine plan (updated Feasibility Study planned) with a less than 10-month payback at spot metals prices. It's also worth noting that a discussion in a recent presentation by Skeena suggested that the company could look at slightly more selective mining to pull grades above 4.0 grams per tonne gold-equivalent vs. the 3.87 grams per tonne gold-equivalent estimated in the 2022 Feasibility Study. If successful, this could lift production further, with annual GEO production increasing closer to 450,000 GEOs in its first five years.

(Source: Company Presentation)

Meanwhile, regarding permitting and financing, Skeena aims to complete its project financing this year and hopes to receive its JA1 Permit by summer so it can begin site earthworks later this year. The company also recently announced the signing of the permitting Process Charter, which is a collaboration between Skeena, the Government of British Columbia, and the Tahltan Nation, with target timelines of the Environmental Assessment Certificate being received in H2 2024 and final permits being issued in H1 2025. Assuming these timelines are met successfully, which looks to be a reasonable assumption, this conforms with Skeena's aim to see its first production by the end of 2025. So, among the developer space, Skeena is one name that is closer to reaching production and certainly is de-risked from a financing standpoint, with it having the ability to finance mostly with debt due to the rapid payback on this project. This compares favorably to other names in the United States that could have lengthier timelines ahead due to being less advanced than Skeena and also subject to rigorous permitting processes. So, for investors interested in a developer that will be spitting out free cash flow by mid-decade with a relatively clear path to production, Skeena is also unique in this aspect.

Valuation

Based on ~85 million fully diluted shares and a share price of US$5.95, Skeena trades at a market cap of $506 million. This is a significant discount to its estimated After-Tax NPV (5%) of ~$1.07 billion for Eskay Creek in its most recent FS, which is based on not only conservative metals prices ($1,700/oz gold, $19.00/oz silver), but what also could be near-peak inflation for some commodities and what I would argue to be limited capex risk due to benefits outlined earlier (limited earthworks requirements, brownfields site, existing tailings storage facility). If we use what I believe to be a fair multiple of 0.75x P/NPV to reflect Eskay Creek's world-class economics, scale, and Tier-1 jurisdiction, I see a fair value for the stock of $803 million [US$9.45].

(Source: Eskay Creek Technical Report)

While this price target already points to a significant upside from current valuations (59% upside to fair value), it does not include Skeena's 40% interest in the high-grade Snip Project (assuming Hochschild spends ~$77 million by 2025), nor does it include an increase in ounces and improved strip ratio in some areas of the mine plan plus the potential to add new zones like the 23 Zone). Lastly, this fair value assumption assigns zero value to near-mine and regional upside, which looks likely given that Skeena enjoys one of the highest-hit rates sector-wide, and it assigns no value to the underground potential at the project with Eskay Creek also boasting an underground resource of 280,000 gold-equivalent ounces at 5.4 grams per tonne gold-equivalent (which excludes newly identified mineralization 650 meters down dip of the NEX Zone in Eskay Deeps). Even if we add just $300 million in value for these opportunities, Skeena's fair value increases to $1,103 million [US$12.98 per share] or US$12.25 per share to be more conservative. This assumes one small equity raise ahead of project financing is completed this year, which could increase the share count to 90 million shares on a fully-diluted basis.

Finally, if we look at Skeena from a free cash flow standpoint once it heads into production, the company is even more undervalued, with the company set to generate over $425 million in free cash flow at gold prices below spot levels in its first year of full production (Q2 2026-Q2 2027). This figure makes up over 80% of Skeena's current market cap, and there's no reason that a company with Eskay's production profile and margins can't trade at a 10% free cash flow yield. So, while we will see more share dilution along the way, as I would expect the project financing to include a mix of debt and equity, Skeena could easily command a market cap of $2.0+ billion long-term, which would still be below what Newcrest (NCM.ASX) paid for Pretium ($2.8 billion) despite Skeena arguably having a more robust project (350,000+ GEOs at sub $700/oz AISC for Eskay vs. Brucejack's ~325,000 gold ounces at sub $900/oz AISC). Hence, no matter how we slice it, I see considerable upside for Skeena long-term, as long as the company can secure its mining permits, with this being the major box left to check for this story.

Summary

With Skeena owning arguably a top-5 undeveloped gold project globally (not held by a major producer) that's located in a Tier-1 jurisdiction, I continue to see it as one of the most attractive juniors sector-wide. This distinction gives Skeena two paths to an upside re-rating, either through bringing the project online itself, which it's very capable of doing with the addition of Randy Reichert, or if the company receives a takeover offer. The latter may seem less likely in a period of capex blowouts on greenfields projects, but Skeena's Eskay Creek is a brownfields site, and after two years of significant inflationary pressures that have put a dent in margins sector-wide, this is a project with scale, meaning it could help a potential suitor to claw back lost margins by reducing a large producer's consolidated costs (Eskay Creek's estimated AISC of $650/oz is nearly 45% below the industry average AISC for major producers).

Given these unique attributes, I continue to see Skeena as one of the best ways to play the gold sector through the developer space. In summary, I would view sharp pullbacks below US$5.45 [C$7.25] as buying opportunities, with this representing what's likely to be a level of strong support for the stock.

Disclosure: I am long SKE, GOLD

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.