It's been a solid start to the year for investors in the Gold Miners Index (GDX), with the index outperforming the Nasdaq Composite (COMPQ) for its second consecutive year despite what’s been one of the best starts to the year for the Nasdaq Composite in a decade. However, while several precious metals producers have put up solid performances and even some juniors have been resurrected, a few are still scraping along their lows and unable to make any real upside progress. Some investors might have concluded that those left behind are of lower-quality and not worthy of betting on, and this is certainly a fair assumption for 95% of the sector given that barely one in ten thousand projects end up becoming mines even in a favorable commodity price environment. That said, one name looks to be a clear exception and is an example of value hiding in plain sight. This company is Marathon Gold (MOZ.TSX/MGDPF).

(Source: Company Presentation)

Despite the recent gold price strength, the easing of inflationary pressures, and fact that it’s ~90% financed and has already begun construction with one of the highest-margin future production profiles in North America, it’s trading at a valuation reserved for a non-permitted and non-financed junior with a mediocre project. In fact, at today’s prices of US$0.64 and even assuming 7% share dilution in addition to the current share count (~537 million fully diluted shares) and using a more conservative 8% discount rate which is more appropriate for developers today given the higher cost of capital and interest rate environment, the stock trades at just 0.79x P/NAV using a long-term $1,900/oz gold price assumption. Let’s take a closer look at why this is far too cheap a valuation, and why this looks to be a low-risk area to start a position in the stock:

All figures are in United States Dollars unless otherwise noted.

The Valentine Gold Project

Marathon Gold’s Valentine Gold Project is in Newfoundland, with Marathon Gold (“Marathon”) having a significant land package of ~24,000 hectares, a surface lease that covers ~2,100 hectares and plans to add 500 hectares to include the Berry pit to add a third pit into its mine plan on top of the previously defined Leprechaun and Marathon pits. The project is located just 60 kilometers from Millertown and will benefit from low-cost hydroelectric power 40 kilometers north of the project at the Star Lake generating station, and its three current pits are spread out relatively evenly across its vast land package, with the potential to add further ounces at Berry and Marathon at depth and what I believe to be a high probability to make an additional economic discovery elsewhere on the property in due course. This could extend the mine life and push out the use of stockpiles, providing a moderate boost to NPV depending on the grades of any new discovery.

(Source: Company Website)

One of the unique attributes of Marathon’s Valentine Gold Project is that these are high-grade open pits, with an average measured & indicated grade of 1.90 grams per tonne of gold, and a reserve base of ~2.70 million ounces at 1.62 grams per tonne of gold (51.6 million tonnes of ore). This is roughly 50% above the average open-pit grade in North America, resulting in Valentine being capable of producing ~195,000 ounces per annum in its first 12 years and ~202,000 ounces in its first six years at all-in sustaining costs of ~$1,050/oz (first six years), and closer to ~$1,010/oz from 2025-2036. Plus, this is despite a relatively modest plant size, with plans to start at ~2.5 million tonnes per annum and increase to ~4.0 million tonnes per annum. Finally, it’s important to note that while upfront capex increased considerably from previous estimates to ~$347 million, this is quite modest compared to other undeveloped gold projects in Canada that are in construction or heading into construction, such as Goose at $480+ million (inflation adjusted due to dated study), and Windfall at ~$600 million, and Marathon’s estimates were done at levels of peak inflation.

Risk Of Further Cost Creep?

One reason that some investors might be steering clear of Marathon Gold is that they’re worried about a repeat of what we saw at Magino (AR.TSX/ARNGF) and Cote Gold (IMG.TSX/IAG), with massive capex blowouts relative to initial estimates which resulted in significant share dilution for Argonaut and considerable divestments and reduced project ownership in the case of Iamgold. However, there’s a few important distinctions to make here that suggest the risk of any significant cost creep is very unlikely. For starters, the most recent 2022 Feasibility Study was done based on more current pricing assumptions vs. Iamgold and Argonaut that had very stale estimates when they saw their capex blowouts. Secondly, we`ve already seen a significant increase in estimates for Marathon, so one could argue that the dreaded capex blowout is in the rear-view mirror and the stock has already been justifiably punished for that disappointment.

Finally, and most importantly, this is a smaller scale project than Cote Gold and Magino with a throughput rate of ~6,900 tonnes per day at the onset vs. Magino and Cote Gold built at ~10,000 and ~35,000 tonnes per day, respectively, and inflationary pressures appear to be easing based on commentary from one of the world’s largest gold producers, Agnico Eagle Mines (AEM.TSX/AEM). These last two points are quite important because the smaller scale suggests less chance of a material cost creep given that this isn’t a monster project like Cote Gold, and the latter point suggests that some assumptions for initial capex may have been too high if updated pricing was done in a period of peak inflation and we see minor easing of some cost inputs and continued weakness in the Canadian Dollar. In fact, the Canadian Dollar has averaged $1.35 USD/CAD since construction began, above the $1.33 USD/CAD estimate, with equipment purchases in USD based on a $1.33 USD/CAD figure.

Updated Feasibility Study: The costs are expressed in Q3 2022 Canadian dollars and include all costs related to the Valentine Gold Project (e.g., mining, site preparation, process plant, tailings facility, power infrastructure, camp, Owners’ costs, spares, first fills, buildings, roadworks, and off-site infrastructure).

As noted above, and per Agnico Eagle’s most recent Q1 2023 Conference Call, we finally received the positive news that inflationary pressures are easing, with the company stating that prices were cooling off for steel, diesel, electricity, and some consumables. This is quite positive for Marathon Gold which is just getting started on major construction at its Valentine Gold Project, with this suggesting that a very low risk of further cost creeping above the ~$347 million upfront capex estimate. In fact, in a perfect world, we could see the company deliver at or marginally below this capex estimate, with a ~$29 million contingency baked in. Still, to be on the safe side, I have assumed a 5% higher cost to build the project (~$364 million vs. ~$347 million), which doesn’t assume any benefit from the favorable trends we’re seeing regarding costs as of Q1 and doesn’t assume any benefit on operating costs either.

“We are seeing some relief, frankly, on the inflationary side, we were talking to our procurement team the other day. And we are starting to see from the -- frankly from the merger with Kirkland Lake. We said it would take a while for some of this to come through. Some of that is starting to come through with some of the new procurement contracts the team has been working exceptionally hard on that. We had some currency tailwinds that help us. So, I think we're very comfortable with the guidance that we have with costs.”

- Agnico Eagle CEO, Ammar Al-Joundi, Q1 2023 Conference Call

Project Economics & Schedule

If we assume a conservative $1,850/oz gold price assumption, more conservative estimates for sustaining capital and upfront capital and a more conservative discount rate of 8% vs. the industry standard of 5%, the After-Tax NPV (8%) comes in at ~$375 million. Using these same assumptions and a $1,900/oz gold price, this increases to ~$433 million. If one prefers to use a 5% discount rate, the net present value of the project changes considerably, with an NPV (5%) of ~$670 million at a $1,900/oz gold price. This is more than double Marathon’s current fully-diluted market cap ($322 million), nearly double its more conservative fully-diluted market cap ($344 million) which assumes 34 million shares of additional share dilution before the first gold pour to address the minor funding gap and it’s worth noting that this places zero value on ounces outside of the mine plan (2.36 million ounces in the M&I and inferred categories), and it factors in the negative impact of warrant/option exercise without any positive benefit of the cash proceeds if warrants and options are exercised. Hence, I would argue this is a brutally conservative way to value the project and the company.

(Source: Company Website)

As for the project schedule, Marathon hopes to send its first ore to the mill by year-end 2024 with its first gold pour in Q1 2025. This means that while its inevitable graduation to producer status was quite far away as of last year, we’re now just over 18 months away from the first gold pour, a catalyst that should drive a significant increase in the share price with producers typically being valued at much higher multiples than developers. And as of the most recent update, nearly 200,000 hours were worked at site with no LTIs, overall project progress was 2% ahead of schedule (24% vs. 22%), and ~$86 million had been spent with ~$142 million committed, with Marathon having $175 million available on its senior secured term loan facility and ~$100 million in cash. So, the company is clearly making solid progress and tracking on plan to its schedule coming out of the coldest and wettest months (February and December), and more favorable weather conditions on deck for project construction.

Valuation & Technical Picture

Based on an assumed 537 million fully-diluted shares and a share price of US$0.64, Marathon Gold trades at a market cap of ~$344 million which pales in comparison to even a very conservative NPV (8% - $1,850/oz gold price) of $375 million. If we add an additional $112 million in fair value which I would also argue to be conservative (1.40 million M&I ounces at $80/oz which assumes minimal exploration upside) and use a fair multiple of 1.0x P/NAV, this translates to a fair value for Marathon Gold of $487 million [US$0.91 per share]. This points to a 43% upside from current levels, but this is based on a brutally conservative valuation while Marathon is a gold developer and should be valued using a higher discount rate.

If we look at the stock from a cash flow standpoint and where it may be valued once it graduates to producer status, the stock is significantly more undervalued, with a fair value of $782 million (NPV 5% - $1,900/oz gold price + $112 million in value for 1.40 million M&I ounces) or US$1.46 per share. This points to a 128% upside to fair value to its 18-month price target, and this would still leave it undervalued from a cash flow standpoint, with this project set to generate upwards of $135 million in average annual free cash flow per annum in its first three years at spot prices. After dividing this figure by today’s market cap, Marathon trades at a ~39% FY2026 free cash flow yield, and even using what I believe to be a fair value of $782 million, this still translates to a very reasonable free cash flow multiple of 5.8. In my view, and even as a single-asset producer, Marathon could easily trade at 10.0x free cash flow in a gold bull market when we tend to see more favorable multiples, and one could argue that we’re in a gold bull market today.

So, while Marathon may be sitting out this bull move in miners and some may be skeptical of a re-rating in juniors, Marathon is a name with clear catalysts that justify it should trade much higher in the next 1-2 years.

Meanwhile, if we look at another avenue to a re-rating (potential takeover), Marathon is significantly undervalued in a period where other jurisdictions are becoming less attractive and suitors are paying up for attractive and simple projects in favorable jurisdictions. This is evidenced by Corvus (Nevada), Great Bear (Ontario), and Sabina (Nunavut) being acquired for an average of $140.30/oz on M&I resources and Great Bear didn’t even have a resource, but I’m assuming an 8.50-million-ounce eventual M&I resource to be proven to give Kinross (KGC/K.TSX) the benefit of the doubt. In Marathon’s case and using its current mineral inventory of ~3.96 million M&I ounces, this would point to a fair value of ~$556 million or US$1.04 per share, making Marathon a highly attractive takeover target for cashed up intermediate producers that might be looking to increase their diversification across assets, add a high-margin operation and add exposure to Tier-1 jurisdictions given that companies with this profile and lower costs are clearly trading at premium multiples, like Alamos Gold (AGI.TSX/AGI).

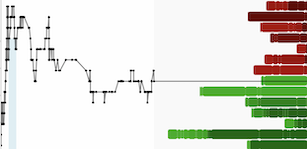

(Source: TC2000.com)

Lastly, if we look at the technical picture, Marathon Gold appears to be under accumulation, with a significant increase in volume with multiple closes well off its lows after a significant correction in the stock. Obviously, there’s no guarantee that these lows hold, and I may be interpreting this incorrectly, but I see the current setup as quite favorable, and it’s always a positive when sentiment is in the gutter which sets a stock up to charge higher once we see a turn in sentiment. So, with a very attractive valuation, the stock hanging out near its lows in what looks to be the mid-point of a multi-quarter base and a surge in volume, I see this as one of the best setups in the junior gold space. Hence, if I were looking for an area to put capital to work in the sub $500 million market cap space with the potential for an accelerated re-rating if we see a takeover offer, Marathon looks to be one of the better bets currently, and the stock is a steal below US$0.64.

Disclosure: I am long MOZ.TSX/MGDPF, AEM.TSX/AEM

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. This article is provided for informational purposes only and is not intended to be investment advice of any kind, and the author is not sponsored by any company discussed in the article, nor has he ever been compensated/sponsored by any company in the sector. Given the volatility in the precious metals sector, position sizing is critical, so when buying small-cap precious metals stocks, position sizes should be limited to 5% or less of one's portfolio.